The fourth quarter was characterized by differences between the major economic power blocks. In Europe it was relatively quiet where France was downgraded. That this news had already been digested by the market was reflected in the prices of French government bonds, which barely moved on the announcement. The ECB left interest rates unchanged at 2%.

In the US, the government “shutdown” initially left the markets unmoved. After the end of the shutdown later in the quarter, macro figures were published again and showed that unemployment is rising again. In addition, bankruptcies were announced with banks and private credit funds taking substantial losses. Threatening import tariffs for China came on top, causing investors to spook, resulting in a brief wave of selling. A trade deal calmed tempers, but volatility increased. The Fed cut interest rates to a range of 3.5%-3.75%.

In Japan, there were concerns surrounding that country’s sovereign debt. Despite a stimulus package, the yen sank further. Investors also saw that the central bank of Japan raised the short-term interest rate (from 0.5% to 0.75%). As a result, Japanese bonds went on sale and the yen also lost further ground (6% versus the euro).

Commodities became more expensive across the board, but the differences between them were large. For example, prices of sugar and oil fell sharply (just under 10%), where prices of gas and gold actually rose by similar percentages.

DC Fund Investments

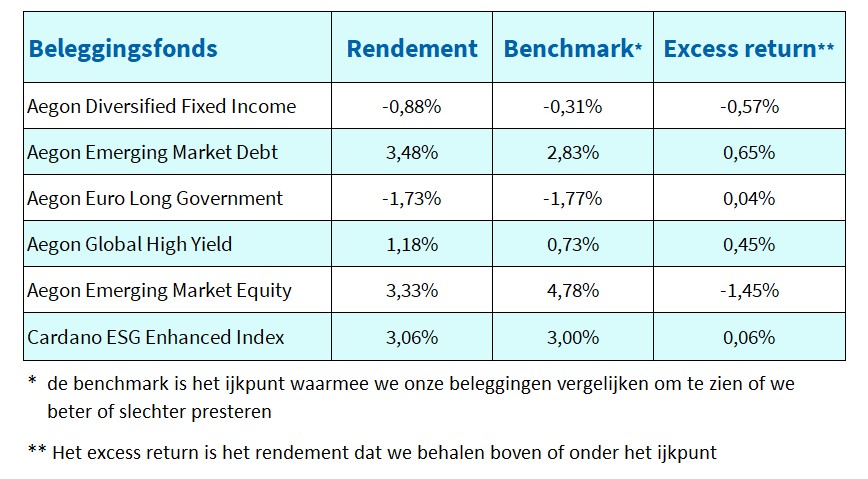

Aegon Diversified Fixed Income

This mixed fund (government bonds (10%), corporate bonds excluding financials (40%), and Dutch residential mortgages (50%)) achieved a slightly negative return in the fourth quarter, and on a relative basis it also lagged behind the benchmark. The contribution of government and corporate bonds was nil, and thus it was entirely attributable to mortgages. This is explained by a larger increase in mortgage rates than Dutch government interest rates. Thus, due to the inverse relationship of interest rates and bonds, higher interest rates mean lower rates.

Aegon Emerging Market Debt

EMD benefited from a lower risk premium by investors over government bonds (from 2.16% to 1.9%). The fund’s higher risk profile, compared to the benchmark, also provided additional returns. Investments in Argentina, Ecuador, Ukraine, Ivory Coast contributed positively to relative returns. Senegal, Malaysia and Mexico underperformed the benchmark.

Aegon Euro Long Government

In the fourth quarter, interest rates on euro swaps and European government bonds continued to rise, resulting in negative returns for the fund. For longer maturities, the increase was stronger than for shorter maturities. Interest rates on Dutch government bonds rose less sharply than on German government bonds. It was also noticeable that the increase on euro swaps was considerably higher than for both countries. The differences were 0.1% and 0.15% for German and Dutch government bonds, respectively.

Aegon Global High Yield

Global High Yield outperformed government bonds as a category, partly due to the shorter maturity of the bonds. Higher risk appetite among investors was virtually unchanged from the third quarter. The fund outperformed the benchmark and this was mainly due to the financials and consumer cyclical sectors. The breakdown in credit quality also worked out well for the fund.

Aegon Emerging Market Equity

Emerging market equities closed the year strongly: the fourth quarter again delivered returns close to 5% for the benchmark. This meant that emerging markets outperformed developed markets for the full year. The positive sentiment around AI and tech continued and that was the main contributor to the absolute return. On a relative basis, this unfortunately leaves the fund behind the benchmark due to the lower weighting of these sectors in the portfolio compared to the benchmark. This is because managers believe that the valuations of some companies in this sector have risen too much. The commodities sector also performed well. This is due to increased demand for (precious) metals as a result of heightened geopolitical tension. Due to an underweight relative to the benchmark, this sector also had a negative contribution to the relative return.

Cardano ESG Enhanced Index

At the end of the fourth quarter, developed markets were 3% higher than the previous quarter. Europe was the best performing region with a handsome plus of 6.3%; significantly better than North America (2.6%) and Pacific excluding Japan (0.0%). On the sector front, healthcare and commodities were the leaders. The fund outperformed the benchmark by a rounded 0.1%. A positive contribution came from stock selection within the communications sector, and the largest negative contribution came from stock selection within the industrials sector.