The first quarter of 2026 was marked by major geopolitical tensions with impact on international financial markets. January started relatively stable with record highs for the AEX and strong performance of emerging market equities. Tightness in the interest rate market around the introduction of the Future of Pensions Act (WTP) was held back by a balanced transition; as a result, fluctuations in interest rates remained limited. However, as the quarter progressed, volatility (movement of rates) increased markedly. Especially after on Feb. 28 America and Israel launched military actions against Iran. This caused a sharp rise in the price of oil (+55%, measured in euros), which was directly reflected in rising inflation and interest rate expectations (especially on shorter maturities). This turmoil led to greater volatility in stock markets, especially in March when equities – especially in emerging markets – came under significant pressure. During this period, energy and utilities held their value better than sectors such as technology and consumer goods. The U.S. dollar also held firm, appreciating 1.6% versus the euro at the end of the quarter compared to the previous quarter.

DC Fund Investments

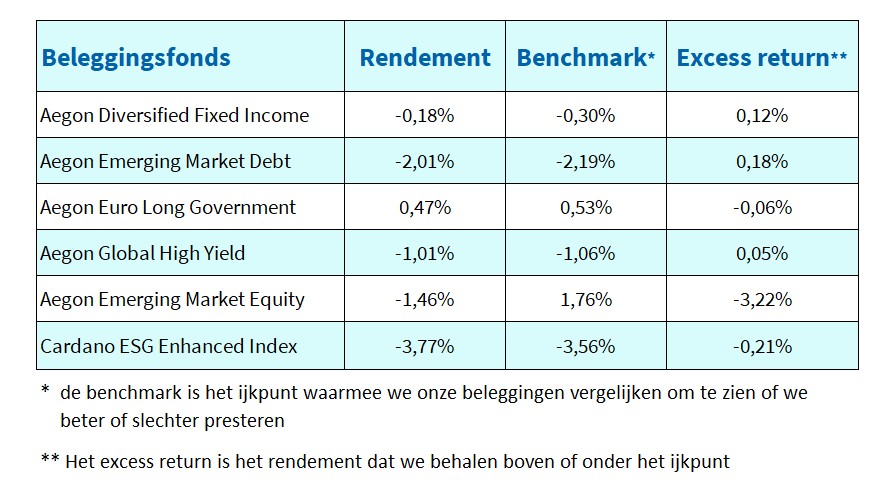

Aegon Diversified Fixed Income

This mixed fund (government bonds (10%), corporate bonds excluding financials (40%), and Dutch residential mortgages (50%)) produced a slightly negative return in the first quarter of this year, but did slightly better than the benchmark on a relative basis. This was entirely due to the relatively good performance of Dutch residential mortgages. Aegon believes the mortgage market is still in good shape. In particular, this is characterized by higher house prices, low arrears and virtually no loan losses.

Aegon Emerging Market Debt

Mounting geopolitical tensions caused a higher risk premium for EMD. Relative to government bonds, it increased by 0.37% to 2.27%. This partly explains the negative (absolute) return over the first quarter. However, most of it was caused by hedging the currency risk. Compared to the benchmark, the fund still has a slightly higher risk profile (in terms of credit rating), but this was reduced slightly in the past quarter. Underlying managers managed to make a positive difference compared to the benchmark with some individual investments.

Aegon Euro Long Government

The first quarter saw a flattening of the yield curve, with shorter maturities rising relatively hard and longer maturities falling slightly. For example, 5-year Dutch government bond yields rose 0.30% and 30-year yields fell 0.11%. This is due to increased inflation expectations, which is caused by the sharp rise in oil prices. Apart from the 30-year rate, German government bond yields rose slightly less than Dutch government bonds.

Aegon Global High Yield

A higher risk premium in Global High Yield caused this category to underperform government bonds. The unrest in the Middle East reduced investors’ risk appetite considerably. The fund slightly outperformed the benchmark (+0.05%), which is mainly attributable to the cash position (related to currency hedging) in the fund.

Aegon Emerging Market Equity

The performance of this category was remarkable in the first quarter. It started strongly with fairly high positive returns in January and February. However, March (-11%) was a very poor month and on balance a small plus remained for the index. The fund fell short of that by more than three percent. On the one hand, this was due to the underweighting of certain tech- and AI-related stocks; of these, the underlying managers feel that valuations have risen too much. On the other hand, it was the underweighting of the energy sector that cost returns relative to the benchmark.

Cardano ESG Enhanced Index

Equities developed markets also saw a mixed picture in the first quarter. January and February still showed modest gains, but March saw a correction on earlier gains. With a return of -3.77%, the fund underperformed the benchmark by 0.21%. The fund invested a smaller weight than the benchmark in the energy sector, which performed strongly last quarter. However, it did invest in the better performing companies in that sector, which more than made up for the relative loss relative to the benchmark.