Notes Uniform Pension Statement 2026

Every year you receive a Uniform Pension Statement (UPO) from us. The UPO shows how much pension you have accrued to date and approximately how much you will receive when you retire. You also see what is arranged for your partner and/or child(ren) after your death and what you can count on if you become unfit for work.

Below are some items from the UPO that we highlight in extra detail. Are you looking for other information, for example about your factor A? Then take a look at our frequently asked questions.

- Starting in 2025, you will see the capital to be achieved on your DC-UPO. This is the capital you are expected to build up with the premiums that have already been deposited as well as the premiums you will continue to deposit and invest until your retirement date.

Important to know: this amount is not yet a pension benefit. On your retirement date, you convert this capital into a pension. How high that pension will be depends, among other things, on the interest rate and life expectancy at the time of conversion.

Therefore, estimating the pension to be reached gives you a better idea of what you can actually expect later.

- On your UPO, you can click through to more information about our investment policy at “Learn more” under the heading “Investing for your retirement. Here you will also find information on SRI.

- On your DC-UPO, we are required to include information about our policy coverage ratio. However, this coverage ratio says nothing about the development of your DC capital. It only says something about the funding of DB pensions.

- Are you joining IBM or Kyndryl for a second time? Then you will no longer receive separate UPO(s) for both employments. We will add your pension from both employments together. The information on the increase of your pension includes the supplementary scheme of your current employment. It is therefore possible that part of your pension has a different allowance scheme.

Additional explanation

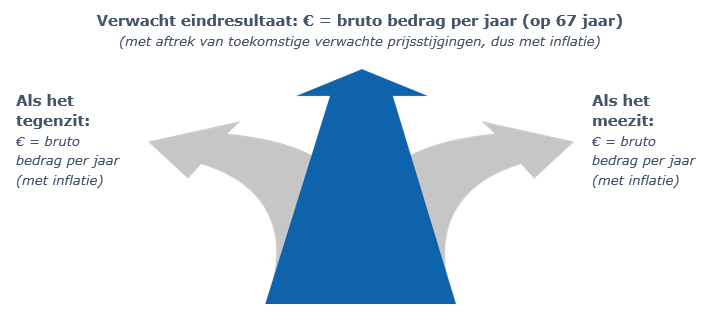

What if it’s up or down?

The UPO shows how much pension you will receive if things go well or badly. You can see this in the picture with the arrows. Here you can see this picture, with some extra explanation.

You can use the upper amount to check whether the expected pension will be enough for you to live on later. For example, you can compare this amount with your current salary.

The amounts on the left and right indicate the direction in which your pension may develop if the economy is very good or bad. The three possible outcomes also take into account future price increases (inflation). As a result, the amounts are different than under the heading “What pension can you expect?” (on the UPO). See below under Rising prices for more explanation. In all four outcomes, the DC-UPO takes into account the purchase of retirement pension and partner’s pension in the ratio 100:70. The DB-UPO does not take this into account. The division between between your old-age pension and partner’s pension is not automatically fixed. Are you going to retire? If so, please indicate in your pension choices what division you want for your retirement and partner’s pension. Have you divided your pension with your ex-partner? The amount you see here has already been reduced by the portion for your ex-partner. If you stop working, you remain entitled to the DB pension and/or DC capital you have accrued.

It’s a good idea to log into the Pension Planner from time to time (say, every year) so you can see the direction your pension is going.

Rising prices

As prices rise, we all suffer loss of purchasing power: we can buy less with the same amount of money. The amounts in the picture with the arrows already take the price increase into account in the expected pension amounts. On our website we explain what we are doing to maintain the value of DB pensions. We also explain there how you can think about purchasing a variable or fixed pension for DC, for example.

Personal data => accrued pension at state pension age

Are you over 65 and still working at IBM? Then in your personal data you will see a pension accrued at state pension age. In the past you accrued a pension that would normally start at age 65. Because you are now over 65, this pension has been recalculated to a pension at state pension age.

Areyou divorced and have divided your pension with your ex-partner?

On your DB-UPO you will see in your personal data your retirement pension at age 60, 65 and/or 67. The pension for your ex-partner has already been deducted from these amounts. How much pension have you accrued?” shows your pension at your state pension age. The first line shows your total pension including the pension for your ex-partner. The second line shows what part of your pension is for your ex-partner. How much pension will you receive if you continue to accrue?” shows your pension including future accrual and excluding the pension for your ex-partner.

Do you have both a DB pension and a DC capital? Then in the letter accompanying your UPOs, we already add up the amounts for you. The pension for your ex-partner has already been deducted from these amounts. So here you only see the pension accrued so far for yourself.

Are you out of service and have a DC capital? Your partner is entitled to this after your death

If you have left employment and only built up a DC capital, the UPO indicates that the partner’s pension after your death is €0.00. However, your DC capital becomes available to your dependents after your death to buy a pension with with an insurer or other provider. We cannot indicate on the UPO what the expected amount of this pension is, because this depends, among other things, on the age of your partner, the purchase rates of the insurer or other provider and the amount of your capital at the time of your death.

Making additional contributions to your DC plan

Do you have a DC plan? Then you can deposit extra for a better pension. If you are already making extra contributions, your extra contributions are included in the accrued amounts shown on the UPO. Would you like to know more, or also deposit extra in your DC scheme? Then go to the Pension Planner in MySPIN.

Pension for yourself (old-age pension) versus pension for your partner in the event of your death (partner’s pension) In “What pension can you expect?” we take into account in the amounts old-age and partner’s pension in the ratio of 100% state to 70%. This is an assumption. If you then look at ‘What will your partner and children receive if you die, however, you may see € 0 there. This is because here we do not work with assumptions, but we assume the actual amount.

Think with us!

For your retirement, you may make some important choices. Clear communication is only natural then. That’s why a participant panel reviews our pension communication in advance. Is our message clear enough so that you know you have to make choices, what choices you have to make and how you make them? We are still looking for DC participants for the participant panel. Would you like to sign up? Then send an email to redactie@spin.nl.